Electricity distribution networks: Creating capacity for the future

To deliver these social and economic benefits, there must be a step change in the approach to the distribution network. This will require investing proactively in the network through greater strategic planning and simplified price controls that take account of a wider range of objectives. This should deliver greater benefits to consumers – and see them realised earlier – as well as helping to manage the transition to electrification more efficiently over time. Reforms will also be required to enable faster deployment of network infrastructure, as well as better customer service for households and businesses looking to connect to the grid.

Demand for electricity is set to increase as heating, transport and industry increasingly turn to electricity to decarbonise. The National Infrastructure Commission’s analysis for the second National Infrastructure Assessment projected demand for electricity would increase by around 50 per cent by 2035 and double by 2050.

All households, and the vast majority of businesses, connect to the distribution network. And around a third of generation is connected to the distribution network – a proportion which is growing as more solar and onshore wind is deployed. Not all this power will need to be used locally. Distribution networks will also need to be able to export some power to other parts of the country via the transmission network. Significant value will also be created from consumers responding to price signals to use their electricity when clean power is plentiful.

It will be critical that the network is able to meet the expected level of future demand and maintain a reliable electricity supply to all consumers. As reliance on electricity increases, networks must be resilient to climate change and security of supply must be maintained.

Inevitably, there is uncertainty around exactly where and when new sources of demand will connect to the network. However, the objectives of achieving net zero emissions, expanding house building and growing the economy create confidence that increased network capacity will be needed in the medium to long term – especially as electrification is the best option for decarbonising an increasingly large proportion of the economy. Waiting for demand to materialise risks investing too late, creating bottlenecks and delays. Proactive investment in the network will ensure that capacity is available when it is needed to support decarbonisation and the wider economy.

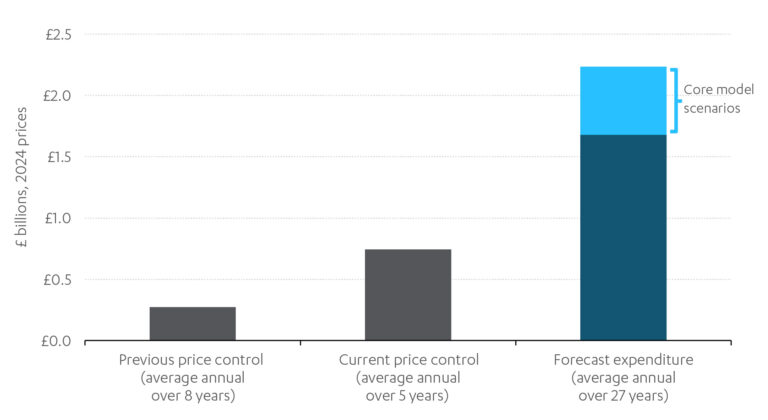

Nationally, £37-50 billion of investment in the distribution network could be needed to support additional demand and generation between today and 2050. This represents at least a doubling of current annual allowances for load related expenditure, on top of business as usual investment, such as end of life asset replacement (see Figure 1).

Figure 1: A step change in electricity distribution network investment is needed

Average annual load related expenditure from 2015 to 2050

Sources: Commission analysis using Regen and EA Technology’s modelling and data from the Department for Energy Security and Net Zero and Ofgem.

Note: This excludes non-load related expenditure. Forecasts have been uplifted for 132 kV load related expenditure using Department for Energy Security and Net Zero forecasts and for low voltage service cables load related expenditure using Ofgem data.

Consumer led flexibility, such as rewarding consumers for charging electric vehicles at times of lower demand, will be an important part of the future energy system and bring significant potential benefits for households. Flexibility is expected to be key to meeting the government’s mission to deliver clean power by 2030 and its ambition to meet net zero by 2050. Maximising consumer led flexibility could reduce the amount of investment required in the distribution network by around 15 per cent and even greater savings could be made from avoiding the need to build generation and transmission network capacity beyond that required. Changes to network management processes, increased digitalisation of the distribution grid, better designed price signals to customers and smart technology in homes and businesses are all required urgently to allow the value of flexibility to be delivered.

Significant changes in how networks are planned and regulated will be needed to deliver the required level of proactive investment efficiently and effectively. This includes strategic planning of energy supply and demand to provide more certainty on the needs case for investment. Ofgem’s proposed Regional Energy Strategic Plans should provide this. However, they must be implemented in a way that provides certainty over investment for the next price control period and beyond. They also need to be set up in a way that delivers clear accountability, strong engagement with local stakeholders and integrates national and local objectives.

Price controls will need to be reformed to enable proactive investment. The current regulatory process is too complex and focused on the short term cost of network investment, rather than the wider goals of economic growth and decarbonisation. Continuing the current approach risks delaying investment and putting significantly more pressure on networks and supply chains in future, as well as on the bills of future consumers. Ofgem should rebalance the price control around a broader set of long term objectives. These should include enabling economic growth, accelerating progress towards net zero, strengthening network resilience and delivering high quality customer service.

To deliver the increasing number of new and modified distribution connections required, improvements to the connections process and customer experience will be needed. Reforms aimed at tackling the connections queue and significantly reducing connection times are ongoing. This process should provide benefits for distribution network customers, but the general process of connecting to the network also needs to be improved. All network customers should receive a high quality customer service, supported by a clear process and consistent good practice. Stronger incentives encouraging networks to deliver the major connections needed to support economic growth will also be required.

Ambiguities and outdated regulations in the planning system can act as a blocker on the maintenance and expansion of the distribution network. A small number of targeted changes to the planning and consenting regime for distribution infrastructure would speed up delivery and reduce uncertainty for both planners and network operators.

Supply chains and workforce capacity need to be more actively managed to speed up project delivery. There are increasing pressures from inflation, stronger global competition and longer lead times, as well as competition for skills across the energy sector and wider economy. Strategic planning and price control reform can help manage these challenges by offering greater certainty around the need for forthcoming network investment. But proactive interventions to meet current and future skills gaps are urgently needed. This must include measures to attract, recruit and retain the large workforce needed to deliver the energy transition.

To achieve this, the Commission recommends eight system-wide reforms:

- Going further and faster on digitalising the network and deploying flexibility in a way that maximises national benefits for the electricity system and for consumers

- Reviewing security of supply standards so that networks are designed appropriately for future loads

- Developing more effective strategic planning to enable and de-risk proactive investment, including Regional Energy Strategic Plans that align stakeholders around a clear trajectory for the future needs of the network

- Reforming and simplifying price controls by:

- rebalancing them around long term objectives that deliver wider social and economic benefits, as well as efficient delivery

- reorientating funding mechanisms to focus on allowances set before the price control begins, using re-opener mechanisms only where there is genuine long term uncertainty

- accelerating ‘no regrets’ activities such as unlooping and off-gas grid reinforcement.

- Government adjusting its relationship with Ofgem to provide the necessary steers and vision to enable proactive investment, including by strengthening the strategy and policy statement

- Improving the connections process through the introduction of minimum service standards and stronger incentives for major connections, to ensure high quality customer service and timely connections for all network customers throughout the full connections process

- Making targeted reforms to the planning and consenting system to speed up the delivery of distribution infrastructure and reduce uncertainty for operators

- Government should urgently identify the skills challenges and actions required to ready the workforce to deliver the energy transition.

A changing role for distribution networks

The distribution network is critical for meeting net zero and enabling economic growth

The distribution network is an essential component of our electricity system. It is how all households, and the vast majority of businesses connect to the network, as well as around a third of generation – a proportion which is growing as more solar and onshore wind is deployed. Sufficient capacity on the distribution network is a critical enabler of economic activity. Timely connections allow businesses to set up and expand where they want to. The network must also remain reliable and resilient, maintaining security of supply as demand grows, while also adapting to a changing climate.

The distribution network is also critical to decarbonisation and reaching net zero. Having sufficient network capacity is essential to the electrification of heat and transport. It will also be key to meeting the ambitious levels of flexibility required to balance supply and demand – such as through smart electric vehicle charging – required by government’s clean power by 2030 mission. New types of economic activity, such as data centres and advanced manufacturing, need significant and reliable electricity supplies. Existing industrial activity will increasingly join them in electrifying. The government’s ambitious housing targets will also require access to reliable and timely electricity connections if they are to be delivered.

It is certain that network demand will increase, but not certain where and when change will happen

Electricity demand on the distribution network has been static or declining for many years – domestic electricity consumption in the UK fell by 26 per cent from its peak in 2005 to 2023. However, the transition to net zero will make the energy system increasingly dependent on electricity, with demand for electricity expected to increase by around 50 per cent by 2035 and to double by 2050.

The projected growth in embedded generation – generation which connects at distribution – will also require network growth. The National Energy System Operator estimates that the volume of distribution-connected generation will increase from around 30 GW to between 80 and 140 GW in 2050. Consequently, the ability of the distribution network to link supply and demand – including where power needs to be exported to other parts of the country via the transmission network – will be increasingly important.

The decisions of individual households and businesses will determine when demand increases in specific locations. But we can be confident in aggregate future demand rising in the long term because it will be required to meet the legally binding target of decarbonising the economy. Increased confidence in the electrification of heating and surface transport means there is greater certainty about the level of future demand than there was at the start of the current price control period.

From steady state to proactive investment

Taking a more proactive approach to investment

While the system has been in a steady state, there have been strong arguments for focusing on efficient management of the distribution network and minimising the risk of over-investment. However, as the network begins a period of significant change and expansion, an approach focused on minimising network costs will not work. It risks consumers missing out on wider social and economic benefits – like meeting decarbonisation targets and enabling economic growth. It may also fail to deliver the investment needed to maintain reliability and sufficient resilience to the impacts of climate change. The current ‘just in time’ approach to investment also does not do enough to ensure the efficient transition to net zero over time and across subsequent price controls.

While the current price control has seen an increase in load related expenditure, a step change is now required. The Commission’s analysis shows that to meet increasing demand between today and 2050, around £37-50 billion of investment in the distribution network is required. This is at least a doubling on current annual rates, with investment needing to accelerate most steeply in the next five to ten years.

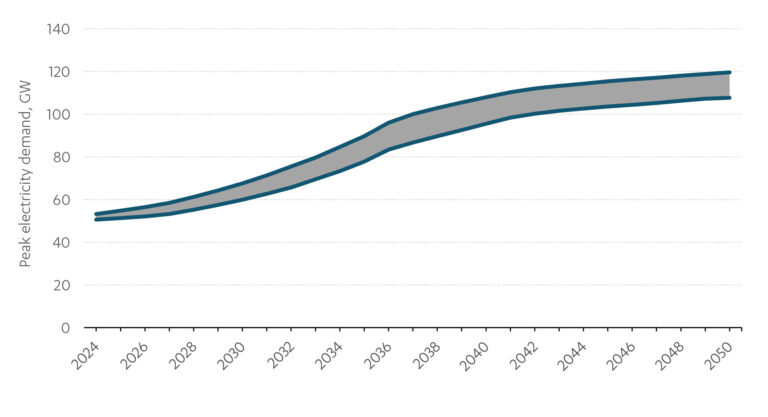

Moving to a proactive approach and delivering this level of investment will require adopting a greater short term risk appetite, as it will not be possible to fully resolve all uncertainty before investment decisions need to be taken. As demand on the distribution network grows, the nature of the risks around proactive investment will change. With steady demand, the challenge is to avoid investing too heavily ahead of need, resulting in stranded or underutilised assets. But with demand expected to grow rapidly – particularly in the 2030s – there is now greater risk from falling behind need (see Figure 2). The risk of assets not being required is limited and any underutilisation should be temporary.

Figure 2: Electricity demand is expected to accelerate through the 2030s

Peak electricity demand from 2024 to 2050, core model scenarios

Sources: Regen and EA Technology’s analysis for the Commission, using Electricity System Operator’s Future Energy Scenarios 2023 and the second National Infrastructure Assessment in combination with distribution network operators’ data.

A step change in investment will require short term risks to be taken, but remaining reactive rather than proactive will worsen the challenges around connecting to the network when it needs to become easier for generators, new housing and growth industries to connect. A reactive approach also risks slowing the pace of decarbonisation if network capacity is not there when consumers need it.

A proactive approach can better balance risks over the medium and long term up to 2050. It can also support a more programmatic approach to investment, rather than looking at specific projects and needs cases on an individual basis. This will ease the supply chain and skills challenges for network operators by providing the market with certainty that sustained, increasing demand for parts and workers will materialise. A programmatic approach will also enable distribution network operators to build strategic partnerships with suppliers and contractors to deliver more efficiently over time.

While significant network investment will be required in the next price control period, plans must remain flexible and adaptive over subsequent price controls. This will allow lessons to be learned and the benefits of innovation to be captured, as well as adjust the investment pathway as certainty grows over time.

The consequences of failing to meet changing patterns of supply and demand have become clear at transmission level. Network connection dates have been pushed out significantly. In 2023, energy bill payers paid £1.4 billion in constraint costs because the transmission network did not have the capacity to transmit all the energy generated by renewables. The lack of capacity on the transmission network has had knock on impacts for the distribution network too – around 40 per cent of the distribution connections queue is dependent on transmission reinforcement. Failing to meet changing patterns of supply and demand must not happen on the distribution network as well.

Flexibility is crucial for Great Britain’s energy system but ‘flex first’ is not

Flexibility is the ability for something connected to the electricity system to adjust when electricity is used or produced – either in time or location. Flexibility broadly takes two forms: national flexibility, used to reduce the size of peak demand and balance supply with demand, and local flexibility, which is used to manage pinch points in networks by moving demand in parts of the network close to capacity to lower demand periods where grid flows are faster.

Maximising the use of flexibility across the electricity system will enable more efficient system management. Deploying flexibility further and faster will also reduce the costs to consumers by reducing the amount of generation and network infrastructure that needs to be built to meet increased demand. The government’s Smart Systems and Flexibility Plan estimated that increased flexibility could reduce total system costs by £6-10 billion per year in the run up to 2050. The modelling in this report shows that consumer led flexibility could reduce required distribution network investment by around 15 per cent.

The government’s 2030 Clean Power Plan requires 10-12 GW of consumer led flexibility as well as additional battery storage. To support this, the planned Low Carbon Flexibility Roadmap must focus on maximising flexibility where it is the best system wide solution. This should include the implementation of digital systems needed to support this and allowing all consumers to benefit from facilitating it, including market wide half hourly settlement, which Elexon is programme managing.

Government and Ofgem will also need to ensure that the distribution network is designed to support this increase in flexibility. Currently, distribution network operators follow a ‘flex first’ approach, deferring or avoiding investment where it is lower cost than building new infrastructure. While the ‘flex first’ approach could be justified while electricity demand has been relatively stable, it is not appropriate in a world of rapidly increasing demand.

Continuing to use flexibility while deferring investment could result in a bottleneck for network reinforcement while demand growth is accelerating rapidly. There is also a risk that local flexibility could come into conflict with national flexibility if demand is shifted to suit local network needs when a different investment or action is more valuable or efficient for the system overall.

While further analysis may be required to fully understand these dynamics, investment in the distribution network will be required to ensure that it is possible to realise the full benefits that national flexibility can offer. Flexibility to deal with local network challenges will remain useful where it can provide an enduring solution or time to plan and coordinate investments more strategically. Prioritising national flexibility should provide even greater benefits.

Recommendation 1 – Government should introduce measures to maximise the use of flexibility across the electricity system, working with the National Energy System Operator and Ofgem to deliver the Low Carbon Flexibility Roadmap by the end of 2025. This should cover the role of flexibility and digitalisation across all parts of the electricity system, including:

- working with Ofgem to update the smart meter rollout plan by the end of 2025, including measures to fix smart meters not currently operating in smart mode

- implementing the smart appliance mandate for heat pumps in 2026

- working with Ofgem and Elexon to deliver market-wide half hourly settlement by 2027 without further delay

- supporting industry to improve flexible asset registration.

Maintaining the reliability of the network

Great Britain’s electricity distribution network is very reliable. Reliability has increased significantly since the 2010s and power cuts are rare events for most consumers. As demand on the network increases – especially as heat demand transfers from gas to electricity – government and Ofgem will need to work together to ensure that a high level of reliability is maintained in an economic manner, with security of supply standards updated to reflect this.

Commission analysis for the study included a ‘winter stress test’ scenario which combined high future heating demand with low levels of flexibility. This scenario suggests that investing to the full peak of future demand in accordance with current security standards could add over £25 billion to the amount of distribution network investment required between now and 2050. While this scenario illustrates the importance of managing peak demand and deploying flexibility, investing to this level would not be prudent. Instead, the focus should be on maximising flexibility to avoid the need for this level of investment.

This scenario also demonstrates the need to consider whether security of supply standards for the network need updating. Current security of supply standards assume low levels of flexibility and low diversity of demand, as well as low levels of digital network capability and smart device integration. Sensible investment and modelling of these new features should lessen the amount of network build required to maintain a high level of security of supply. Therefore, the role of flexibility and ‘smarter’ solutions will be important to consider, alongside additional investment in maintaining security of supply.

There will also need to be a strong focus on wider network resilience and its capacity to anticipate and respond to shocks and stresses such as extreme heat, storms and flooding. In a changing climate, the network must be designed for the conditions it will face in 2050 and beyond. Much of this can be delivered through clearer objectives and incentives in the price control process. But network operators will also need to develop and cost adaptation plans, as the Commission recommended in the second National Infrastructure Assessment. Alongside this, Ofgem should incorporate climate risk into its asset risk metric as the Commission set out in its Developing Resilience Standards in UK Infrastructure report.

Recommendation 2 – Government and Ofgem should review security of supply standards for distribution networks to ensure that they are designed for future loads and vulnerable customers are protected.

As part of business planning for the next price control:

- Ofgem should require distribution network operators to identify ‘no regrets’ activities that would improve security of supply

- government and Ofgem should work with distribution network operators to agree the detailed work required to review security of supply standards and how this will be undertaken.

The full review of security of supply standards should then be completed by the end of 2028.

Reforms to support proactive investment

Strategic planning

To enable the proactive investment required to deliver a distribution network fit for net zero, there should be a step change in the way that the network is planned. A more strategic approach is needed to support the maintenance and upgrades that must be delivered to achieve government’s decarbonisation targets.

The governance of the UK’s energy system is undergoing significant change to move it in this direction. The recent launch of the independent National Energy System Operator – formerly the Electricity System Operator – represents a new approach to the running of the network and a wider move toward increased strategic planning. Reflecting the need for regional considerations, Ofgem has confirmed that the National Energy System Operator will introduce new Regional Energy Strategic Plans. The Commission welcomes this decision, having supported their introduction in the second National Infrastructure Assessment. These plans are intended to support coordinated development of the system and enable long term investment to be made with confidence and ahead of need. They will also look beyond the distribution network, aligning electricity and gas, with scope to potentially include heat, hydrogen and other vectors.

These changes to the governance of the energy system should help clarify the roles and responsibilities for organisations across the system, which will be critical to achieving clean power by 2030 and net zero by 2050. If network operators produce investment plans that are consistent with the Regional Energy Strategic Plans, Ofgem’s role can become more focused on assuring timely and efficient delivery of network investment. It is important that the shift toward strategic planning streamlines the governance system rather than adding complexity. It should also provide better data that can support more effective and innovative planning across the sector and wider economy.

It is critical that the roles and responsibilities of all parties involved in the development of Regional Energy Strategic Plans are clear and resourced appropriately. In particular, local authorities must be able to input into their development meaningfully so that regional plans take appropriate account of local plans and priorities. Support will need to be given to local authorities with relatively lower capacity and capability to ensure regional plans have democratic accountability. Their involvement can help prioritise what is most important and ensure credible local priorities are supported.

Recommendation 3 – Ofgem and the National Energy System Operator should set out a clear statement of accountability for the Regional Energy Strategic Plans. This should include the decisions that the system operator will be empowered to take in developing the plan, how they will assess network investment plans in a proportionate way, and the stages at which different actors will have the ability to input and challenge.

Recommendation 4 – Ofgem and the National Energy System Operator should develop structured ways for local authorities and other local stakeholders to input into the Regional Energy Strategic Plans.

- The National Energy System Operator should proceed with plans to make tools and advice available to local stakeholders to support their planning role. Government should also assess what additional capacity and capability is required for local authorities to engage meaningfully with the process and provide the necessary financial support for them to do so.

- Local authorities must have structured mechanisms to input meaningfully into Regional Energy Strategic Plans, even if they are not on the strategic board or have not completed a formal local energy plan.

- Local decarbonisation targets and strategies should be enabled as far as reasonably possible, where projects are underpinned by credible plans for delivery.

Recommendation 5 – Ofgem and the National Energy System Operator should use the Regional Energy Strategic Plans as a vehicle to improve planning and data in the sector. As part of the process, the National Energy System Operator should:

- develop a register of projects ‘in development’ that have not yet had connection applications submitted

- publish the plans in both an open data format, and through a publication that is accessible and understandable to all energy system actors, including local government.

Recommendation 6 – Ofgem and the National Energy System Operator should set out a proportionate transitional plan for the Regional Energy Strategic Plans to inform the next electricity distribution price control. This should be delivered far enough ahead of decisions about the price control to enable network business planning. It should give network operators confidence in the investment pathway for the whole price control period as well as an indication of the longer term trajectory of investment.

Price control reform

Price controls set the amount of money that network companies can recover from consumers over the price control period. Ofgem, as the regulator, sets price controls for the companies that operate Great Britain’s gas and electricity networks at both distribution and transmission level. Distribution network operators submit business plans to Ofgem outlining their estimated costs for operating and building their networks during each price control period. Ofgem then assesses these costs and sets baseline revenue allowances. Distribution network operators then maintain and operate the electricity distribution network and recover their revenue through charges in consumer energy bills.

Ofgem designs the framework with mechanisms and targets to drive efficient performance and incentivise distribution network operators to deliver outcomes that benefit consumers.

The current electricity distribution price control period runs from 2023 to 2028. Early indications are that network operators have not yet significantly increased load related expenditure to prepare for higher future peak demand, despite a rise in allowances from the previous price control. A slow start at the beginning of a price control period is not unusual and there have been persistent underspends in the early years of past price controls. This is due to a range of uncertainties, such as the take up and impact of low carbon technologies, as well as supply chain challenges and natural turbulence around the start and end points. To meet the demands of the transition to net zero and government’s goal for economic growth, it is important that proactive investment begins to be delivered during the current price control period. Beyond this, price controls will need to be reformed to enable the further proactive investment required.

While the fundamental principles of the price control framework – using incentives and innovation to drive outcomes – should be maintained, the process is too complex and too focused on minimising short-term costs at the expense of wider consumer value. Future price controls need to be orientated around a clear set of rebalanced objectives, including enabling decarbonisation and economic growth and improving customer service as well as maintaining the reliability and resilience of the network. Investing ahead of need should also mean that the growing number of consumers seeking to install heat pumps and electric vehicle charging points in their homes can do so at the time of their choosing. Minimising consumer costs through appropriately incentivising efficient delivery will remain important. However, solely focusing on minimising the amount of investment will not represent value to consumers and could come at the expense of a more cost efficient transition to net zero over the long term.

Funding mechanisms also need to be reformed to achieve these outcomes. Under the current framework, uncertainty mechanisms are used to scale up network investment during the price control period where Ofgem judges there is not sufficient certainty to commit to it at the start. Ofgem’s approach to the uncertainty around low carbon technology uptake has been to introduce a larger volume of uncertainty mechanisms, with the number of ‘re-openers’ common to all network operators doubling during the previous price control, from eight to 16.

Continuing the current price control model will limit investment certainty and carry a high administrative burden for companies and Ofgem, slowing decision-making. Instead, Ofgem should allow more upfront funding, with re-openers used only where there is genuine and material long-term uncertainty. More clarity and certainty over long term investment should help build confidence and provide visibility for the supply chain. Network operators can then secure the supply chain and workforce requirements needed to enable proactive build and stay ahead of need. Higher allowances will need to come with additional mechanisms to ensure distribution network operators actually invest in new infrastructure and that value for consumers is maintained.

As part of ongoing maintenance and renewals, network operators should be funded to take a ‘touch the network once’ approach by installing assets that are future proofed for future higher levels of demand. This approach is already starting to be embedded and extending it further should minimise costs and disruption over the long term by avoiding the need for assets to be replaced multiple times. Wider ‘no regrets’ investment activities also need to be accelerated. Proactive unlooping of domestic properties will remove a barrier to the installation of low carbon technologies, where households would otherwise have to wait an extended period to install a heat pump if their boiler breaks down.

Recommendation 7 – Ofgem should base future price controls around a rebalanced set of objectives focused on long term requirements for the distribution network that deliver wider consumer value, alongside consumer costs. These objectives should include Ofgem’s net zero and growth duties, as well as strengthening network resilience and delivering high quality customer service, including connection outcomes. Funding mechanisms and incentives should be designed to deliver these objectives.

Recommendation 8 – Ofgem should orientate the next price control around allowances set before the price control begins. Funding mechanisms should be set at a sufficient level to enable proactive investment. This should include:

- using re-opener mechanisms only where there is genuine long term uncertainty and the process and objectives for re-openers is proportionate to the investment being considered

- setting allowances to enable a ’touch-the-network-once to 2050’ approach as standard, to build resilience and minimise the overall costs of investment to deliver net zero.

Recommendation 9 – Ofgem should accelerate no regrets activities such as proactive unlooping and off-gas grid reinforcement. Government should also set a date for the elimination of looped supplies to inform Ofgem’s approach to delivery and enable distribution network operators to develop a programme for completing the work across multiple price controls.

Government and Ofgem

To successfully transition to a model of greater proactive investment – and deliver the reforms to strategic planning and price controls which enable this – it is important that the relationship between government and Ofgem is appropriately adjusted. Ofgem’s role in the governance of the network has become more complicated. It has new duties to support meeting net zero in 2050 and promote sustainable economic growth, which it did not have at the start of the current price control.

With an expanded and more complex role, Ofgem needs a clear sense of which objectives it should prioritise. But government currently lacks the powers to provide Ofgem with a suitable strategic vision. The most recent strategy and policy statement set out 15 strategic priorities and 32 policy outcomes which government wished to achieve.

Government should adjust its relationship with Ofgem so that it can provide the necessary steers to enable proactive investment. Government should do this by strengthening the strategy and policy statement to provide a clearer strategic vision, as well as considering whether the current legal framework gives government sufficient ability to direct Ofgem on strategic matters. Any changes should be limited to strategic steers, not individual regulatory decisions, so that Ofgem’s independence is maintained.

Recommendation 10 – By the end of 2025, government should provide a stronger strategic vision to Ofgem through an updated strategy and policy statement. This should include clarity on a more focused set of priorities and outcomes for the energy sector, that better reflects government’s objectives and the trade-offs between them. The revised strategy and policy statement should include the importance of proactive investment in the distribution network.

Removing barriers to an expanding network

Connections

The projected rapid increase in demand for electricity will require an increased number of new and enlarged network connections. All demand customers should be able to easily connect to the network when they need to and priority generation customers must also be able to connect in line with government targets. Otherwise, there is a risk that it will not be possible to connect the right mix of renewables needed to decarbonise electricity supply, to build the new developments required to meet housing targets or deliver economic growth, nor for domestic customers to install low carbon technologies, like heat pumps and electric vehicle chargers.

Moving to proactive investment can ease the connections process by keeping capacity ahead of demand. This will be particularly critical for ensuring the simplest connections are quick and easy – for example, so that distribution networks do not create frictions for domestic consumers fitting a heat pump, or other low carbon technologies, when they want to. However, just maintaining sufficient capacity on the network is not sufficient and the connections process itself also needs to be improved.

At present, the connections queue is too long and some projects applying for a connection today cannot expect to connect to the network for over a decade. This is usually where projects require transmission reinforcement, as capacity issues are more acute on the transmission network. Significant work is currently being undertaken by the National Energy System Operator to reform the connections queue by prioritising those projects which are ready to connect and align with the needs of the future energy system. It will be critical that this work continues at pace.

In contrast, distribution network operators estimate that new projects can typically expect to take between six months and four years to connect to the network, depending on voltage level and requirements for third party consents and/or distribution reinforcement. This variation in connection reflects the different characteristics of projects and the variation in capacity across the network as well as different customer priorities. Not all projects require the fastest possible connection as, for example, developers do not want to pay for a connection years before their project is complete. What is important is that connections are delivered to a timescale that suits the customer and that the process works effectively and predictably.

While many connections processes run smoothly and networks’ customer satisfaction scores are generally high, it is not uncommon for customers to face delays and wider issues with the connections process. Delays to connections can be driven by customer choices and factors outside the control of network operators, but the Commission has heard a number of common issues with the process that are within networks’ control. Network customers of differing sizes, across demand and generation, have repeatedly pointed to poor customer service, misaligned connection incentives, disparities between distribution network operators, and a lack of data as key issues with the connections process. These issues were also highlighted in Ofgem’s end-to-end review of connections.

While distribution connection times (excluding those where transmission reinforcement is needed) are far shorter than the ones currently being experienced on the transmission network, there has been a steady increase in average connection times since the start of the previous control period. It is essential that common challenges are addressed now, before demand increases over the coming years, to avoid the distribution connections process constraining decarbonisation and economic growth.

To simplify the process and ensure all customers have access to high quality, timely service, Ofgem should introduce new minimum service standards, applicable to all distribution network operators. These standards should raise the level of service across all distribution network operators while still providing scope for operators to go above and beyond by tailoring their service for specific customers.

More specific reforms are needed to deliver distribution network major connections, such as housing developments, factories and data centres, as well as distribution connected generation. Given the centrality of these projects to the objectives of the network – and the likelihood that the number of such projects will increase significantly – distribution network operators should be better incentivised to deliver them. It is important that incentives cover the full connections process, including pre-application engagement and the post-offer ‘negotiation’ phase, where customers and distribution network operators finalise their connection agreement. Performance should also be measured robustly and transparently, with appropriate rewards that are proportionate to the ease and timeliness of connections and the quality of service provided.

Recommendation 11 – As part of the next price control, Ofgem should introduce minimum standards for distribution network operators. These standards should include:

- agreed connections guidance for all customer types and all distribution network operators, including indicative pricing and connection timescales

- enabling all domestic customers to apply for the installation of more than one low carbon technology through a single application, regardless of where they live

- developing common digitised connection documentation to be used across all network operators.

Recommendation 12 – Ofgem should strengthen the incentives for delivering major connections in the next price control, with a view to sustaining this approach in future price controls. The reformed incentives should:

- appropriately incentivise performance across each part of the major connections process, including ‘pre-application’ engagement and post-offer ‘negotiation’ phases, through financial rewards and penalties based on clearer performance expectations

- measure distribution network operator performance robustly, with requirements to publish connections performance data, including timeliness of connection offers and actual connections delivery

- offer appropriate rewards for high performance, as well as penalties for poor performance.

Planning and consenting

To meet government’s decarbonisation targets, barriers to the delivery of network upgrades must be addressed. The Commission has previously identified challenges with the infrastructure planning system, including in delivering the transition to net zero, for Nationally Significant Infrastructure Projects. Overcoming these challenges should help speed up delivery of distribution network infrastructure.

However, much of the distribution network does not fall within the Nationally Significant Infrastructure Project regime. The Commission has identified a small number of targeted changes to wider planning and consenting which could help speed up investment in the distribution network. Some of these changes may require primary legislation, but should remove unnecessary bureaucracy and save time for network operators, land owners and local and national government. These changes include clarifying and widening eligibility for permitted development and aligning access rules with those for other utilities.

Recommendation 13 – Government should reform the planning system by the end of 2025 to enable new connections and network upgrades to be made more quickly. Changes should include:

- amending the Overhead Lines (Exemption) (England & Wales) Regulations 2009 and the process for seeking consent under section 37 of the Electricity Act 1989 to allow a wider set of alterations to overhead lines to be made without the need for planning permission

- addressing the ambiguity in the process for acquiring rights in private streets under Section 10 and Schedule 4, Paragraph 1 of the Electricity Act 1989

- amending Schedule 6 Paragraph 9 of the Electricity Act 1989 to extend access for operators conducting maintenance activities on third party land, so that they can cross as much land as is necessary, when that route is the most efficient

- amending the Town and Country Planning (General Permitted Development) (England) Order 1995 to increase the volume threshold for substations to be built with permitted development rights from 29 cubic metres to 45 cubic metres.

Supply chain and skills

Like many other sectors, the distribution network faces supply chain and skills pressures. As demand on the distribution network grows and investment increases, these pressures are likely to grow. As well as the challenges common to other sectors, there is increased global competition within the international energy market. While supply chain pressures currently pose a more significant problem for the transmission network – where global competition is most acute – some of this equipment is also common to distribution networks. Global competition is also likely to move to distribution network equipment as transmission investment is completed.

Taking a longer term, proactive approach to network investment can help manage these pressures and support manufacturers and their supply chains to plan for volume increases. A more strategic approach to procurement, informed by a longer term view of distribution network investment plans, could enable network operators to make stronger commitments to their supply chains who, in turn, can plan for the increased volume of parts needed. Government and Ofgem should also consider whether new mechanisms that have been developed to manage the transmission supply chain could also be applied or adapted for distribution networks.

Skills shortages impact the whole of the energy sector and pose a significant challenge for the deliverability of the energy transition. For distribution, the most significant concern is a shortage of craft skills, particularly cable jointers and overhead line workers. There are also concerns that general engineering skills and growing requirements, such as digital and data, will not be met. There is strong competition for these skills within the energy sector, with other infrastructure sectors and across the broader economy, which makes it difficult to solve issues specifically within the distribution sector.

Given the time it takes to develop these skills, urgent action must be taken to ready the workforce for the energy transition and to meet net zero. Short and medium term solutions – such as retraining and recruiting skilled workers from other countries – can help, but they will not be sufficient to manage the long term workforce challenge. Government needs to review the issues and identify the actions required to address skills challenges. This should inform a wider net zero skills strategy that sets out how the workforce will be developed and maintained over time.

Recommendation 14 – Government should identify the skills gaps and actions required to attract, recruit and retain the large workforce needed to deliver the energy transition. This should form the basis of a net zero skills and workforce strategy, published by the end of 2025.

Infographics

link